1. No Sales!

Fee-only financial planners provide expert advice and assistance and will never sell you any financial products. We know that some planners offer “free” financial plans. We do not. But we also know that there is no such thing as a free lunch—there is a cost for that “free” plan and you will likely be very surprised what the real cost is to you.

2. We Work For You.

A fee-only financial planner has a legal fiduciary responsibility to work solely on your behalf, in your best interests, without any conflicts of interest.

3. Planning for Anyone, Regardless of Your Wealth.

Our fee-only, hourly services enables us to work with clients interested in assessing and improving their financial situation regardless of how much money you currently have. We don’t manage money so we have no minimum investable assets requirements. However, our Pierside Service Program clients must meet some financial criteria to make the program feasible for them to join.

4. Planning for What You Need, When You Need It.

A fee-only, hourly rate financial planner can work with you to prepare a full and comprehensive financial plan or, if you prefer, we can address very specific issues regarding your investments, debts, education funding, estate planning documents, insurance or any topic of your choice on an hourly or project fee basis. In short, there is no “one size fits all” solution. Our Pierside Service Program clients have a comprehensive and integrated financial program that addresses these and other issues during the annual service schedule.

5. Highly Qualified Financial Advisors.

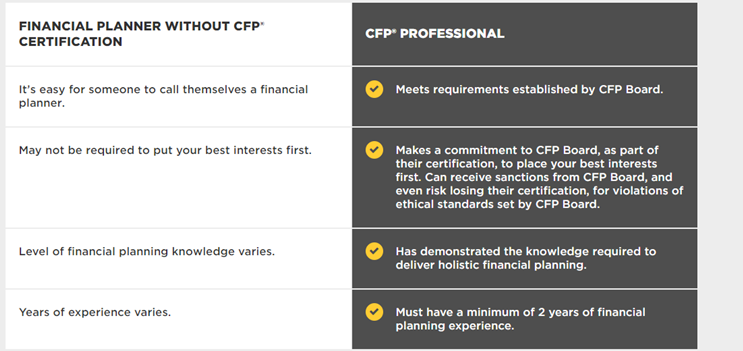

Our firm’s planners are Certified Financial Planner™ professionals who have earned this designation through a challenging program of education, experience, and passing a comprehensive examination. Many people can call themselves “financial planners,” but only those who have earned this designation can call themselves CFP® professionals—the Gold Standard.

6. Want Some Other Opinions on the Value of Fee-Only Planners?

"An adviser should be a Certified Financial Planner, or CFP@professional, just as I am. That means that he or she cares enough about his or her clients to have gone through a two-year certification process, with continuing education requirements mandating that he or she stay up-to-date on the kinds of information that you need... [A good planner] boils down to just 5 words: Someone who doesn't sell products."

-Suze Orman

"With fee-only planners, there is no conflict of interest.The bottom line: Financial professionals make their money through various compensation models, so make sure you ask about any real or perceived conflicts of interest and know exactly how your advisor is being compensated."

-AARP

"Understand the compensation, The planner should be upfront about this. Commission-based planners are paid for the financial products they sell.

Fee-only planners charge a flat fee for all services or a fixed advisory fee plus a percentage annual fee or flat retainer to manage your money. Ask specifically if the planner will provide services with the "duty of care of a fiduciary," meaning they're obliged to base their recommendations on your best interests and to fully disclose any conflicts of interest. If he or she can't answer affirmatively, find another planner.”

-Consumer Reports

"Anyone can hang out a shingle as a financial planner, but that doesn't make that person an expert. They may tack on an alphabet soup of letters after their names, but CFP (short for certified financial planner) is the most significant credential and is a good sign that a prospective planner will give sound financial advice. Consider the planner's pay structure.

You typically want to avoid commission-based advisers.Planners who work on commission may have less than altruistic incentives to push a certain life insurance package or mutual fund if they're getting a cut of that revenue."

-Wall Street Journal

Why you should work with a Certified Financial Planner™

When you hire a CFP® professional, you work with an advisor who has met rigorous qualifications for financial planning. Most important, a CFP® professional has made a commitment to CFP Board to act in the best interests of their client.

A CFP® professional works with their clients using a comprehensive planning process: